Here is a sampling of print and online articles as well as television segments featuring Elisabeth in her roles as a broadcaster, columnist, money-saving expert and media relations coach.

We’d all like to finish next year with a bit extra in our pockets. The good news is, when your goal is relatively modest, there are plenty of ways to get there. On the following pages you’ll find our best saving and earning ideas—each with the aim of winning you an extra $1,000 in 2018. Few of these strategies are easy, but none will require a major life change. While you are certainly free to give up your daily trip to Starbucks ($3.65 for a grande latte x 365=$1,332.25), we aren’t even going to ask you to do that.

• Rejigger Your Bills

• Lower Your Cost of Living

• Get a Gig

• Hone Your Health Care

• Eat Right

• Control Your Spending

• Cheapen Your Thrills

• Make Your Hobby Pay

• Get There For Less

• Make It In the Market

• Earn More at Work

• Make Money Off Your Stuff

• Get Ready to Retire

• Tackle Tuition

• Save as a Family

Tens of millions of Americans have dropped cable—and for good reason. The average bill hit $103 a month last year, according to the Leichtman Research Group. But there are countless streaming options. A comprehensive package would include HBO Now, Netflix, Hulu, and CBS All Access, totaling around $37 a month, or $444 a year, for a savings of almost $800. Go with just HBO and Netflix and you’ll save $968.

The average family of four’s cell phone bill adds up to about $2,880 a year. But Sprint’s prepaid Family Plan—the cheapest plan we found—is only $1,260.

The average household with credit card debt pays $1,292 in interest a year, according to NerdWallet. A balance transfer can give you a year of 0% APR to help you catch up.

Doing it in a year won’t be easy, but you can get there, says Greg McBride, chief financial analyst at Bankrate. Paying your bills on time is the first step. Also focus on keeping your “credit utilization ratio”—the amount of your credit limit you use—below 10%. Your new, higher credit score could shave as much as one percentage point off your mortgage rate in today’s market, says McBride. That will save you $1,000 a year on a $150,000 home loan.

On a $90,000 parent PLUS loan with a 6.6% interest rate, you’re shelling out $1,025 a month on a standard repayment plan. Refinance to a private loan at 4.5% and you could save $93 a month, says Christine Roberts, head of student lending at Citizens Bank.

The average membership costs $50 a month—and much more for boutique classes like SoulCycle. Try a free fitness group like the November Project, which is active in over 40 cities, or an intramural team through work. If all else fails, Janis Isaman, a nutrition coach and Pilates instructor based in Calgary, Alberta, recommends looking on Facebook and Craigslist to find people nearby who also want to form an ad hoc fitness club.

Adjustable-rate mortgages got a bad rap during the financial crisis, but they can make a lot of sense if you aren’t planning to stay in your home long term. Right now the average 30-year rate is 4.1%, according to Bankrate, compared with just 3.6% for a five-year adjustable-rate loan. On a $300,000 mortgage, that half a percentage point should save you about $86 a month, or $1,032 a year.

“When we redid our bathroom this year, we couldn’t get many contractors to return our calls for such a small project—so we scaled back our plans. We avoided major plumbing, electrical work, or anything else that would require a permit or that our handyman couldn’t handle. Instead, we had him redo all the surfaces: We subbed in new tile, faucet hardware, lighting, paint, and a new vanity. The bathroom looks brand new, but the end cost was half of the single contractor bid we did receive—a savings of more than $10,000.” —Rachel F. Elson

As many as 14.9 million Americans live with a roommate, according to the U.S. Census. It’s easy to see why: In cities like San Francisco, a roommate can save you more than $1,000 a month, per a 2017 report from SmartAsset, a real estate website. In less expensive markets like Detroit, you’ll save over $300 a month with a roommate, totaling almost $4,000 each year.

Homes sold between May 1 and May 15 sell for about 1% more than the average listing, according to a 2017 report from Zillow, translating to an extra $1,500 in your pocket.

Delivery men and women have lots of freedom with Postmates, which allows workers to walk, bike, or drive to deliver goods and food in major cities across the U.S. Log on whenever you want. The company says that you can earn as much as $25 an hour, plus tips.

Uber drivers make an average of $15.68 an hour, according to the popular RideShareGuy blog, though that varies by city and doesn’t include the cost of maintenance or gas (Lyft drivers make even more, $17.50). Still, a few hours each week will easily net you $1,000 by year end.

If you really enjoy building Ikea furniture or don’t mind carrying a couch up three flights of stairs, you can make some serious money on TaskRabbit—about $35 an hour, on average, the company says. Many of the in-demand tasks, like installing shelves or moving furniture, require a skilled hand (or a truck), but if you have the know how you can bank a lot of extra money in your off time.

Blogger Jason Wuerch says he’s earned $10 to $15 an hour filling out online surveys. While Survey Junkie and SwagBucks are the best known, you can maximize your haul by signing up for 10 to 15 and rotating among them, focusing on each site’s most lucrative offers. (Find a list on Wuerch’s site, FrugalForLess.com.) Spend an hour or two a few mornings each week—or work on them during your commute—and you’ll reach $1,000 by year end.

Make money from home by providing feedback on new websites at sites like UserTesting.com, TryMyUI.com, and Userlytics.com, through which you can earn $10 per testing session. SideIncomeJobs.com is another option that has a user fee but guarantees you’ll make $100 in your first 30 days. You won’t be eligible for every testing session, so this is a less steady stream of income than surveys, according to blogger Scott Alan Turner, but it could add up to hundreds of dollars a month.

Whether you’re a writer, designer, or coder, you can sell your skills in your free time at sites like Upwork and Fiverr. Some of the most popular services on Fiverr’s marketplace are graphic design–oriented like creating logos, as well as copywriting and translation services, says a spokesman. Prices vary per project, from $5 for a simple WordPress bug fix to hundreds or thousands of dollars for something like website design.

Retailers hire tens of thousands of extra workers for the holidays, with some gigs paying as much as $16 an hour (although $11 to $14 is more common).

Nationally, babysitters earned $13.97 an hour on average last year, according to a Care.com survey. That means by working 6 p.m. to midnight one Friday night a month you can earn $1,006.

For everyone from retail clerks to housekeepers, job website SnagAJob focuses on hourly work. You can search for part-time jobs and specify when you want to work, like nights or weekends.

Workers with health insurance through their employer pay an average family premium of $467 a month for a PPO vs. $321 for a high-deductible health plan, according to Mercer. That’s $1,752 a year in premium savings. The strategy can pay off even if you aren’t in perfect health. Just make sure you have enough cash on hand to cover your higher deductible.

Paired with high-deductible health plans, these portable accounts allow you to set aside pretax dollars for medical expenses now or in the future. A single person making $60,000 (in the 25% federal tax bracket) who puts away $288 a month in an HSA would save $863 a year in federal income taxes. Once you’re retired, you can use HSA money for Medicare premiums.

22. Deduct your health care costs

22. Deduct your health care costsYou need to itemize, and your medical costs must exceed 10% of your adjusted gross income. You can then deduct any amount you paid above that threshold. If you’re dealing with an illness or injury this year or if your income is particularly low because of retirement, job loss, or a break from work, you’re best poised to claim this deduction.

Nearly all large employers offer wellness programs, and about three-quarters of those offer financial incentives to employees to participate. You can earn money for activities like getting your cholesterol checked or signing up for a workplace exercise program. The average employee incentive adds up to $742, according to the National Business Group on Health. Make a healthy salad for dinner instead of getting takeout a couple of times a month, and you’re up to $1,000.

“You don’t have to be a heavy smoker to waste big bucks on the habit. In New York, the cigarette minimum is $10.50 a pack (some brands cost $14 or more), which at two packs a week carries an annual cost of $1,000. Last year, I left the smoking section for good and saved more than $900. And not a moment too soon: In 2018, the minimum price for a pack in New York City will jump to $13.” —Kristen Bahler

You’ve probably already heard about Groupon’s restaurant, fitness, and beauty deals, but did you know you can also use the site for discounted eye, dental, and chiropractic exams? If you visit the chiropractor twice a month, and your insurance doesn’t pay the average $68 fee (as per Chiropractic Economicsmagazine), you’ll save around $1,000 by using packages advertised on Groupon—which often work out to $25 or less a visit. Just be sure to research each office on Google, Yelp, and social media beforehand. Groupon doesn’t vet its merchants, so if a business doesn’t have a solid Better Business Bureau rating and plenty of good customer reviews, it’s probably worth skipping.

Generally if you don’t sign up for Medicare Part B by age 65¼, your monthly premium increases by 10% for every 12-month period that you’re late. This penalty lasts as long as you have Part B. Most new beneficiaries paid $134 a month for 2017, which means that enrolling a year late will cost you $1,000 extra after just six years.

Prices for medications under Part D drug plans vary widely, even within the same zip code, according to a study by the Senior Citizens League. The price of Ventolin, an inhaler used to treat asthma, varied by $119 a month, for example. Choosing carefully during open enrollment, which runs from Oct. 15 through Dec. 7 each year, could save you $1,400 annually for that one drug.

Want restaurant-quality fare without spending the money for a meal out? Budget meal-kit services, like Dinnerly, can take the hassle out of cooking and save you money if you are willing to skip dining out. A couple spend about $3,000 a year in restaurant and takeout expenses. Dinnerly charges $38.99 for three meals a week—saving almost $1,130 a year.

The typical family of four with school-age children spends $1,054 a month on food, according to the U.S. Department of Agriculture. On average, store brands are 30% to 40% cheaper than famous name ones, says food marketing analyst Phil Lempert. That means, over the course of a year, shaving $1,000 from your grocery bill should be well within reach. One tip: Compare ingredients and nutritional information on the packages. If they are the same, chances are both products are being made by the brand-name company and are basically identical, according to Lempert.

The average menu price for an imported beer is $5, according to Numbeo. In other words, treating yourself and a date to two drinks with dinner once a week will cost you $1,040 a year. Skipping those drinks won’t just save you money, but also thousands of calories apiece.

The average American household throws out between $1,350 and $2,275 in food each year, according to the Natural Resources Defense Council.

Vegetarians save $750 a year, according to the Journal of Hunger and Environmental Nutrition. Those figures still include plenty of pricey ingredients like olive oil. Want to save a bit more? Swap in cheaper alternatives like canola oil.

People who buy lunch every weekday burn through serious cash—about $2,500 a year, if you spend $10 on an average meal. Mona Meighan, author of What Are You Doing for Lunch?, estimates that brown bagging can cut your costs by 80%. You don’t even have to go that far. Swap your $10 lunch-out habit for a meal from home that costs $4, Monday through Thursday, and you will save about $1,200.

84% of us have bought something on a whim. Many of these purchases are $25 or less, but 54% of people say they have spent more than $100, and 20% more than $1,000, according to CreditCards.com. Set up a rule, say a 24- or 48-hour hold period, before you buy anything over a certain price threshold. “We tend to provide a greater weight to current payoffs than future ones, so waiting 24 or 48 hours before making a bigger purchase is an excellent way to overcome our present bias,” says Joe Sterf, a CPA and founder of Average Joe Finance. “Instituting a holding period gives us time to think about the future and not impulsively react. With that extra time, we’ll be less likely to make the purchase.”

You can’t save if you don’t know how you’re spending your money. “By seeing how much money is going in vs. going out, you will be able to make better buying decisions to help reach your financial goals,” says Andrea Woroch, a consumer finance expert. Apps like Mint or PocketGuard help because they make it easy to see which needless purchases you can eliminate in the future. Woroch says most of the wiggle room will probably come from clothing, grocery, and entertainment spending.

“With Digit, you select a goal and a time frame in which to accomplish it (mine is to save $2,000 in the next year for a vacation), and the app saves small amounts of money for you. Digit has a monthly fee of $2.99 after a 100-day free trial, which is something to be aware of, but so far I’ve saved over $400 in just a few months, which I just wouldn’t have done on my own. Plus, I get daily text messages with my bank balances and how far I’m progressing toward my goal.” —Alicia Adamczyk

Research by economists Shlomo Benartzi at UCLA and Yaron Levi at USC found people who downloaded a financial app looked at their account 12 times each month, compared with going to the website twice a month. The results: Spending fell 16% in the four months after people loaded the app, led by less discretionary spending. Dining out expenses dropped by 19%, and grocery bills by 21%. Annual savings on the average grocery bill alone could net you over $880.

The 52 Week Money Challenge is simple: Save an extra dollar every week of the year—$1 the first week, $2 the second week, and so on, until you reach $52 saved in the last week of the year, for a total savings of $1,378. “So many of us don’t deal with money, because we have negative associations with it,” says Kristin Wong, author of the forthcoming book Get Money, who led a similar challenge for Lifehacker.com. “If you can make it fun and empowering to save money, you’re going to actually want to deal with it.”

Try a “no spend” month, or a day each week, by picking a time in which you pay bills but buy nothing except the necessities (groceries, gas, etc.). It may seem difficult, but there are plenty of forums on the web for support—try Reddit’s 12-million-subscriber-strong Personal Finance subreddit, or NPR’s Your Money and Your Life Facebook group, where commenters update their “no spend” challenges daily. “Small challenges lead to small wins, and it’s super empowering to see that you’ve actually saved some cash,” says Wong.

For a family of four, booking flights before Halloween saves about $1,200 on average if you are planning to travel for both Thanksgiving and Christmas or Hanukkah, based on price estimates from Hopper.

Booking early doesn’t save enough? With the average cost of a roundtrip U.S. flight hovering at $367, the rule of thumb is to drive if the destination is less than 500 miles away. A family of four can save more than $1,200—even when you include an overnight stopover.

For your next trip, check out a vacation rental through sites like Airbnb, VRBO, or HomeAway. A recent study found that in 16 of the top 22 cities for travelers, Airbnb stays were cheaper than hotels by an average of $56 a night. That may net only the heaviest travelers $1,000 a year. But in some cities, like London and Paris, the savings were much greater—eclipsing $100 a night. In other locations, including Toronto, Vienna, and Madrid, you could save $90 to $100 on average by renting a room in an apartment where guests share the kitchen and bathroom.

For a weeklong vacation with kids, consider skipping a conventional hotel where you’ll have to book two rooms and instead take advantage of an extended stay hotel like TownePlace Suites or Candlewood Suites. On average, you’ll save $157 a night at this type of lodging—which usually includes a kitchenette and a sofa bed for the kids.

For frequent travelers it can pay to rack up points on a rewards card. Put all of your purchases, especially on dining and travel, on a card like Chase Sapphire Preferred or American Express Platinum, and your miles should save you $1,000 or more a year on flights.

Americans spend more than $70 billion a year on lottery tickets, well over $1,000 per household in some states like Massachusetts ($1,976) and Georgia ($1,211), according to data site Metrocosm. Your chances of winning Powerball: about 1 in 292 million.

The new iPhone X is priced at $999 and up. Don’t buy it.

The average American woman spends $8 a day on makeup and other skin care products, according to retailer SkinStore. The good news: Most women have plenty of unused makeup at home—more than $2,000 worth, according to beauty site escentual.com.

“Ebates.com, a ‘cash back’ site—you can also try FatWallet.com and TopCashback.com—has become part of my online shopping routine. Many brands’ discounts are in the 2% to 3% range—hardly worth my time. But Sephora, one of my favorites, routinely offers 8% off. Next year I’m planning a family wedding—and the 23% off from Flowers.com could save me several hundred dollars. By shopping strategically and taking advantage of other perks ($25 for each friend I sign up) I am targeting $1,000 cash back.” —Veronica Quezada

Publishers pay anywhere from $50 to several hundred dollars for a “complete concept”—the text and the idea for an illustration, says Ron Kanfi, president of gag card company NobleWorks. Carefully research the publisher ahead of time, so that you can write in the house style, then send six to 10 of your best ideas, he recommends.

Whether you cross stitch or handcraft jewelry, the trick to selling your stuff online is promoting it with frequent social media posts and beautiful photos, says Debby McClain, who operates two Etsy shops. “In a huge sea of sellers, you have to make sure you are seen,” adds McClain, who has sold crafts online for 19 years.

Youth sports officials make around $20 a game, says Barry Mano, president of the National Association of Sports Officials. High school referees can earn between $50 and $70, while college game pay starts at over $100. As an initial step, join your local officials association, which will provide training, and begin scheduling games.

Many churches and synagogues pay singers to perform as part of their regular ensemble or for special events. While rates vary, common listings offer anywhere from $50 to $200 for each practice and performance. The easiest way to find such gigs in your area: Reach out to local institutions, and search online ads such as those at choralnet.org.

At $3.08 a gallon—the five-year national average for gas—a 25 mile commute costs about $2,000 annually in gas alone. And while gas prices have been low recently, gas price researcher GasBuddy predicts they will go up in 2018. By alternating the days you drive to work, you stand to save roughly $1,000—and that’s before you factor in tolls, depreciation, and any parking costs. Bring in a third buddy, and the savings climb to $1,300.

Check the value of your car via Kelley Blue Book. If you’re driving an older model that is worth less than 10 times your insurance premium, consider dropping comprehensive and collision coverage, suggests the Insurance Information Institute, which could save you between $375 and $1,500 a year on that item alone, the group estimates. And always shop around for a new policy: According to J.D. Power, consumers who switched insurers saved an average of $388 in 2015.

These days the average car is on the road for more than 11 years, up from nine in 2000, according to the Transportation Department. Resisting the urge to trade in for a newer model will easily save $1,000 in payments.

Keeping your tires inflated could save you $112 a year in gas money, according to one survey by Edmunds—or as much as $800 if they’re severely deflated. Additionally, aggressive driving can lower your gas mileage by anywhere from 10% to 40% in stop-and-go traffic, according to SAE International, an auto industry trade association. With the average American estimated to spend more than $1,500 on gas this year, that’s another $156 to $624 in your pocket.

Buying the most popular model of a vehicle—commonly a Honda or Toyota—may mean you’re paying more than you need to, according to car site Edmunds. There are often comparable, less popular vehicles that cost much less after cash-back incentives.

“We broke down and bought a new car this summer, but only after three months of waiting out dealerships. We wanted a Honda Pilot, and dealers had plenty of models, but all with extra features we didn’t want and which cost $5,000 to $7,000 more. So instead we waited. Two dealers eventually got the base model we were looking for—and one offered to sell it for $1,000 less than the other.” —Brad Tuttle

59. Sign up for pretax transit programs if offered by your employer

Do you spend up to $255 for parking and/or transit a month? For someone making $37,950 to $91,900, that translates into savings of more than $750. If you park and ride, or make more than $91,900, you can easily surpass $1,000.

Ditching your human advisor can save you some money if you’re comfortable with an online, technology-first solution. Robo-advisors like Schwab Intelligent Portfolios and WiseBanyan don’t charge a fee to manage your money, compared with the 1.1% fee, on average, charged by human advisors. If you have $100,000 saved up in your retirement piggy bank, switching could easily net you an extra $1,000 a year.

The average actively managed stock fund charges investors 1.02% of assets a year, according to Morningstar. Popular large-cap index funds, including versions from Vanguard and Fidelity, routinely charge less than 0.1%.

Sick of U.S. stock funds’ anemic 0.8% average yield? International stock funds boast 1.7%.

If you sell now and lock in the loss, you can count it against gains realized on your winners. You can’t buy back the loser for 30 days, but you can buy something similar, a large company stock fund, say, instead of a midcap one. Workers making $37,950 to $418,400 (15% capital gains bracket) will save $1,000 for every $6,667 in gains they offset.

If your market losses exceed your gains, you can also deduct up to $3,000 of capital losses from your income. You need to make more than $190,000 to net $1,000. But even if you earn $91,900 to $191,650 you will still save $840.

Boost your investment returns by tilting your stock portfolio toward small value stocks, which tend to outperform blue-chip names over the long haul. Just remember it’s not a free lunch. Small value stocks tend to be more volatile, meaning steeper bear market drops.

“Most companies will give you a referral bonus if you recommend someone for a job and the company does indeed hire her. The most common referral bonus is between $1,000 and $2,500, according to a 2016 report from WorldatWork, a nonprofit human resources association. (Referrals for clerical positions are typically lower, from $500 to $1,000, the report found.) In 2015 an average of 13% of new hires came from referrals. I recommended a friend from my college paper. She got hired just as I was moving apartments, and the bonus paid for the movers and some new furniture.” —Alicia Adamczyk

While you may think getting a raise is the key to making you happier, research suggests it actually happens the other way around: Fostering a positive attitude in your day-to-day work could help youmove up in your company or land a big project. According to the Harvard Business Review, an easy way to do so could be through simply helping your coworkers. A 2011 study found that people who coordinated lunches and organized office activities were 10 times as engaged at work—and 40% more likely to get a promotion (and a raise)—as those who didn’t.

Job switchers averaged a 4.5% wage increase in 2017, according to ADP. Workers between the ages of 25 to 34 in full-time jobs saw their wages increase the most. Chris Martin, lead data analyst for compensation data company PayScale, says a lot comes down to your job—those in “hot markets,” like software development, will likely see an increase if they switch, while pay for administrative assistants depends on how long they have been with a certain company.

A recent study by Cleveland State economist Vasilios Kosteas found that frequent exercise led to 6% higher pay for men and 10% higher pay for women, on average. Kosteas attributes the wage increase to a boost in productivity that results from hitting the gym routinely.

70. Job hunting? Save receiptsIf you’re looking for a new gig in the same line of work, you can deduct search-related expenses, from résumé prep to travel costs like mileage and lodging to job placement or employment agency fees. The only catch? First-time job hunters, those looking for a position in a different occupation, and those with a large gap between the end of their last job and their current search don’t qualify.

In some cases, earning an extra grand could be as simple as doing nothing but continuing at your current job. Salaries are expected to increase 3.2% on average next year, according to the Economic Research Institute, meaning if you make the average U.S. wage of $49,630, you’ll bank almost $1,590.

Consider yourself a top performer? In recent years more and more companies have been favoring merit raises as a way to get the most out their employees, according to payroll company ADP. The average merit raise for full-time job holders was 4.3% in 2017—or $2,134 for the average earner.

Though not everyone has extra space to rent out, those who do can earn a decent amount of money via platforms like Airbnb. “I pulled in over $800 a month—all from renting out a spare room that was getting no use,” says Kevin Han, who writes the Financial Panther blog. Earnest, a lending company, reports that Airbnb hosts make an average of $924 a month, although the median, which may reflect a more typical experience, is $440.

74. Rent your home for 14 days or lessCash in on a tax exemption by renting your house for two weeks or less. Doing this keeps you from having to pay taxes on any of the income from your short-term rental. Go up to a 15th day and you’ll owe taxes on the whole sum you earned from all rental days. This move can be a major boon to your budget if you live in an area that hosts popular annual sporting events like a major golf tournament, says Draper, Utah, CPA Troy Lewis.

Similar to Airbnb, sites like Getaround and Turo provide marketplaces where individuals can rent out their vehicles. Again, how much you make will depend on your car: A Honda Civic can earn over $367 a month, according to data provided by Turo, while the average monthly earnings for all users is $539, which accounts for insurance costs.

You don’t have to have a super-yacht. Catamarans, sailboats, motorboats, and even kayaks are in demand. Renting your bowrider in Miami could earn you $39 an hour, while a weeklong rental of a deck boat in Seattle could net you $5,000, according to listings on GetMyBoat.

There’s no shortage of sites that want to be the Airbnb for your other stuff. On ShareGrid, professional photographers offer gear for as much as $1,000 a month. If you have a parking space or driveway in a city like Chicago or New York, CurbFlip and JustPark help you find renters—about a third of parking space owners earn $1,000 a year or more, according to CurbFlip. Omni is a San Francisco–based company that stores your extra stuff—from bikes to camping gear to Halloween costumes—and rents it out for you if you opt in.

“Of course it’s possible to make $1,000 at a yard sale,” says YardSaleQueen.com author Chris Heiska. Her tips: Make sure to advertise properly, and if your home is in a remote area, consider renting out space at a location with more foot traffic, such as a local church or synagogue.

It may not seem like much at first, but if you were to fund your IRA on Jan. 1 of each year—and not wait until the IRS deadline on April 17 of the following year—that 15½ months of additional tax-free compounding will boost your nest egg by around $30,000 in additional savings after 30 years, or $1,000 a year.

For middle-income savers, squirreling away money in a retirement account like an IRA, 401(k), or 403(b) can result in big benefits not only for your retirement but also your tax bill. You can claim a saver’s credit for such contributions equal to either 50%, 20%, or 10% of the total you put in this year up to $2,000 (or $4,000 if married, filing jointly) depending on income.

Each year you wait to start collecting Social Security checks, your benefit grows by 6.5% to 8%. If your monthly benefit was $1,300 at 66—the average for that age—waiting one more year will result in $104 more each month or about $1,248 in total for the year.

Most large employers now automatically enroll employees in 401(k) plans, but about a fifth of workers still don’t participate, according to Vanguard. Even agreeing to sock away 1% to 2% of your salary each year can easily net you $1,000, considering most plans boost your contributions with a match—worth up to 4% of your salary, on average.

Merely being enrolled in a 401(k) is a great first step. But it’s not enough to secure your retirement (or maybe even get the full match). A majority of employers auto-enroll workers at a savings rate of 3% or less, Vanguard reports. Up that to 6% and you’ll finish the year with an extra $1,000—plus a lot of peace of mind.

84. Seniors, use age-related tax breaks

Owning a home past age 65 comes with a host of state tax perks. In nearly every state, tax exemptions can lower your home’s assessed value. Most states offer “circuit breaker” credits to give pensioners back some of the real estate taxes they have already paid throughout the year. And finally, in more than 40 states, seniors can capitalize on limits to annual increases in their property’s assessed value, caps on property tax rates, or freezes on assessments.

About 60% of high school seniors filled out the Free Application for Federal Student Aid last year, according to the National College Access Network. But every college-bound senior should be filling out the form. Why? It’s the gateway to billions of dollars awarded in federal and state grants each year, including the Pell Grant for low-income families. The average Pell Grant is about $3,700 a year.

These tend to be less competitive than larger national ones, and checks worth $500 to $1,000 a semester can add up quickly. Start by looking at nearby Rotary clubs, veterans groups, American Association of University Women chapters, Elks clubs, and church groups. Ask your high school’s guidance office for more ideas.

Room and board now cost more than tuition and fees at public four-year colleges, according to the College Board. Reduce the average $10,800 expense by searching for bargains off campus. Even better? Look for a co-op, where residents do weekly chores in return for lower rent. The North American Students of Cooperation says this option can save 20% to 50% off the cost of private market rent in your college town.

Many large companies offer up to $5,250 a year in tax-free tuition reimbursement. That money can pay for part of a second degree or for one-off courses to develop skills in high-demand areas like coding, data analytics, or entrepreneurship. Even if your employer doesn’t have an official program, ask your boss about subsidizing your training. Make sure your pitch includes program costs, an outline of what you’ll learn, and how that will ultimately pay dividends for your team.

“Considering study-abroad programs? Think about going as a foreign exchange student instead. While you may get less handholding, you can avoid the hefty program costs and even tuition in some countries. In college, I attended the University of Southern Denmark through an exchange program. Because higher education is free in Denmark, I spent only $5,000 for five months of housing, food, transportation, and other necessities—less than a third of the $18,000 the International Institute of Education estimates the average study-abroad experience costs per semester.” —Megan Leonhardt

90. Take the American Opportunity Tax CreditRecoup tuition costs by cutting up to $2,500 off your tax bill. Don’t owe that much? You can have 40% of the remaining amount, or up to $1,000, refunded to you. One catch: You can use this credit only for a student’s first four years of college.

91. Take the Lifetime Learning CreditOffset 20% of the first $10,000 of qualified education expenses you or your family rack up and reduce your tax bill by up to $2,000. The best part: This break can be applied to any courses at an eligible school that go toward a degree or credential, or simply to improve job skills—and there is no limit on the number of years you can use the credit. To qualify, your modified adjusted gross income must be below $65,000 for single filers or $131,000 or less for married joint filers.

92. Deduct your student loans

Deduct up to $2,500 of interest paid if your modified gross income is below $65,000 for singles or $135,000 for joint filers. Singles earning up to $80,000 ($165,000 for couples) can claim a partial deduction. This means the most you can expect to save each year is $625. Still, if you hit the max, you can stretch the savings a bit by signing up for autopay with your loan servicer, which should shave 0.25% from your interest rate, netting an extra $10 to $15 a month for heavy borrowers.

With diapers costing 33¢ a pop (Pampers, size 5, on Amazon.com, for example) you can easily save $1,000 by potty training your child at age 2 instead of 3. As recently as the late 1950s most Americans did this, and parents in many other countries still do, says Michelle Swaney, who runs the website thepottyschool.com.

Set up a local babysitting co-op. Amy Suardi, the mother of five behind the blog Frugal Mama, says aim to enlist about five families, at least at the start. It’s “kind of like a fire,” she says. “You have to fan the flames a lot in the beginning to get it going.”

Average cost to attend an out-of-town wedding: $1,184 per couple, says American Express. Take the newlyweds to a Champagne dinner instead, suggests relationship expert April Masini.

The average weekly cost for a nanny: $556, says Care.com. Willing to try someone with a bit less experience who perhaps speaks a foreign language? You can save about $200 a week with an au pair, according to the website.

Activities like gymnastics can easily top $1,000 a year. But you don’t always have to pay full freight. “Call and ask,” says Elisabeth Leamy, host of the Easy Money podcast. “It’s not always on the website.” Leagues that don’t offer aid may still know about government grants. Local city councils near Leamy’s home in the D.C. suburbs offer grants for both low-income and military kids, she says.

“If a venue costs $7,000 on a Saturday, you can most likely negotiate [to lower] that price on a Friday, a Sunday, or a Thursday,” says Norfolk wedding planner Crystal Salazar. For instance, the Kimpton Hotel Eventi in New York City offers promotional packages discounted for weddings on Fridays and Sundays by $36 to $66 per person—meaning for weddings of 100 guests, this could save you $3,600 or more.

Flowers can cost upward of $5,000, according to TheKnot.com. Lower your bill by hanging colored linens on the walls and tables, then combining the flowers you do buy with eclectic vases or a centerpiece, says San Diego wedding planner Nahid Farhoud. Doing so can save about $2,000 for weddings of 100 to 200 guests.

Mixed drinks typically cost $10 to $12 at the bar, while beer costs $6 and wine around $8, according to Farhoud. That means for a wedding with 150 guests, skipping hard liquor can easily save you about $1,000, assuming three drinks per guest. Another tip: Serve tap water instead of bottled—which can run up to $6 a pop at high end venues.

“As a personal finance writer I always took pride in doing my own taxes. But my wife is a priest, which adds a lot of complexity. A pro cost us several hundred dollars, but he not only handled my wife’s situation, he also pointed out deductions I missed—like my union dues.” —Ian Salisbury

We’ve all been there — at the register with an item for purchase and wondering, ‘Can I get this for even less than advertised?’ You may not hesitate to pose the question when buying an appliance, but experts say the art of negotiating for a better price extends to a variety of scenarios.

Art

You’ve perused galleries/studios for that one piece of art that speaks to you. You’ve found it, but can you negotiate with the gallery owner/artist for a better deal? Yes, says Victor Armendariz, owner and director of Gallery Victor Armendariz in River North.

“A collector interested in an artist’s work always has the choice to ask the dealer if there is any negotiation on the price,” he said. “If there is flexibility in pricing we certainly do our best to accommodate the client, either by offering a break on the price or allowing them to pay the artwork out over a couple payments.”

Galerie Waterton owner Francois Grossas agrees that the leverage is always on the side of the collector/buyer when it comes to art.

“Art is not an essential thing, right?” he said, and negotiating in this realm “regularly happens.” “Of course, it depends on the price of a piece of artwork — if it’s affordable (in the $500-$1,000 range), typically there’s no discount, no argument,” he said. “But if you’re talking about several thousand dollars, then yes, buyers typically expect a negotiation on discount or some kind of reduction in price.”

Cars

Perhaps the best-known place to negotiate is the car dealership. Tips on how to finesse deals through negotiating/haggling are plentiful, but are they doable and impactful? Yes, says Washington, D.C., resident and Easy Money podcast host Elisabeth Leamy.

Before you go to the dealership, she said, do two things: get outside financing, and reach out to dealerships’ internet departments. Car financing is another moving part that complicates negotiations. “After you’ve negotiated a price for the vehicle, you can see if the dealership’s financing is any better than your own,” Leamy said.

Internet departments at dealerships can deal with negotiations via phone and email and are often quicker to reveal their best price for a vehicle. “Plus, they frequently strive for volume sales rather than milking each transaction. This can make for a lower-pressure experience,” Leamy said.

Other details to remember: No need to talk price when you first get to the dealership and ask for a test drive; talk price after the test drive, and know what to pay. (Researching on Edmunds.com can give you insight into setting your opening offer and your maximum offer.); talk price, not car payment.

And mention your trade-in after the entire deal has been negotiated. “Reason being, if you mention the trade-in at the beginning, just like with financing, it’s one more number the dealer can use to make the transaction confusing,” she said.

Retail

It would appear retail purchases can be negotiated too. In addition to firms that exist to help consumers with their car negotiating (e.g. Carjojo), there are companies to help you haggle with other retailers (e.g. Treatail).

When trying to get more off from the ticketed price, remember loyalty programs. Knitwear retailer Nic + Zoe, for instance, opened a Highland Park location in October and just started its loyalty program, which will include deals and offers.

“We’re extremely mindful of the fact that our customer wants value in her product and she wants to feel like she’s getting a deal,” said Zoe Chatfield-Taylor, Nic+Zoe’s merchandising director (and namesake).

A loyalty program coupled with an in-store promotion and a simple query to an employee about matching a competing store’s sale could get you a lower price. Don’t be afraid to ask for that which is not overtly promoted. Case in point: Lane Bryant gives extra discounts to teachers who show a valid school ID or pay stub during checkout. But again, the ask is part of it.

“As long as you’re polite and respectful, you can ask nearly anyone for nearly anything, whether it’s for a big purchase or a small purchase,” said negotiation consultant Devon Smiley. “You may not get it, but you can have a discussion about it. The customer doesn’t always have to be right, but they have a voice.”

drockett@chicagotribune.com

Twitter @DarcelTribune

Based on all the festive lights, trees and decorations in big box stores, it’s obvious the holiday season is upon us. This means spending will likely be at an all-time high in the coming weeks, but you don’t have to fall victim to prior years’ debt statistics. Research shows that the average American spent more than $1,100 on gifts, decorations and festivities last year, and women tend to outspend men. Our infographic offers insight into holiday spending trends from prior years, along with top savings tips from your favorite finance experts and bloggers to keep out of debt.

![]()

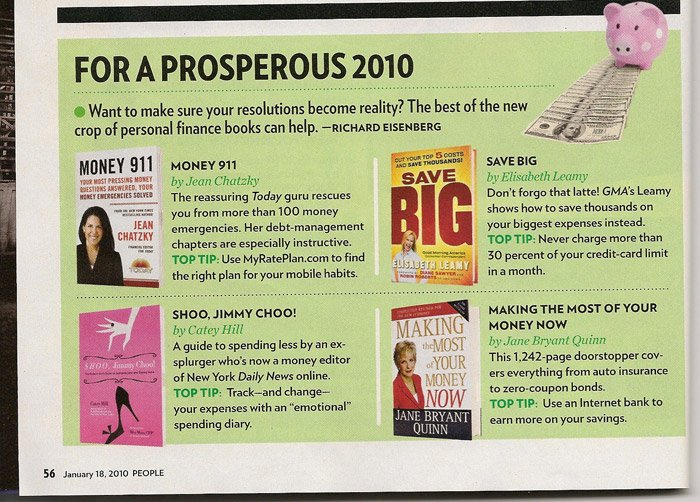

'Good Morning America' correspondent's book offers tips on saving big bucks

Ivan Penn

March 6, 2010

Don't skip the latte! Oh, and inflate your tires — but not to save a few bucks.

Save money, sure. But learn how to SAVE BIG, rather than pinching pennies that will take you a lifetime to accumulate.

Welcome to Elisabeth Leamy's world of how to SAVE BIG, the title of the Good Morning America consumer correspondent's new book. Not that you avoid all small savings tips, but Leamy wants consumers to find big ways to save money faster.

The notion resonates with me because in these troubled economic times we sometimes need a latte, or a spa treatment or a golf outing to ease the pressure. But it doesn't feel like we can (though we later go financially stir crazy and end up splurging).

So I had a talk with Leamy and a look at her book to see how to SAVE BIG rather than small.

Is it possible for everyday folks to do?

"People say to me, 'You're educated. You make good money. I can't do that,' " she said. "I reject that. These big savings steps are not hard to do."

So how does Leamy save big?

Reduce your top five costs, she says, and you'll save thousands. Those include costs related to your home, car, health care, credit and groceries.

Though she pays significant attention to home ownership — about a third of her book focuses on such ideas as selling your house yourself and using tax benefits — Leamy offers something for everyone on how to save, and big.

For example, need a car? Buy a used car instead of a new one and save $10,000 or even $20,000 on the car of your choice.

Sure, you have to do some homework, but the reality is you can find even the nice luxury car for a lot less. While inflating your tires to the right level saves you about $9 a month, Leamy touts some $152,417 in car savings in her book.

"You would have to properly inflate the tires of five cars for 282 years to match that!" she says in the book.

In all, SAVE BIG shows consumers how to save $1,176,916, or the equivalent of about 294,229 lattes.

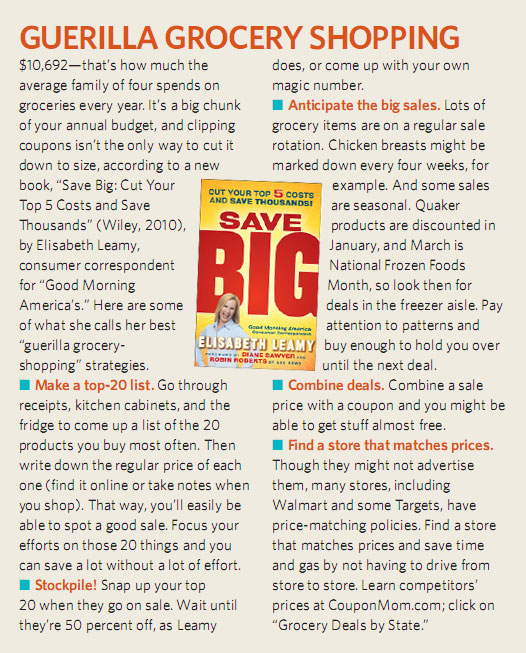

One of Leamy's recommendations that most any consumer can benefit from is her suggestions for grocery savings. Take her suggestion about "price matching." She calls it "our first guerilla grocery shopping weapon."

Rather than running around to different stores to buy items at sale prices, find one store that honors other stores' prices and get everything there.

Some stores will "beat their competitors prices rather than just matching them," Leamy says in her book. "For example, Lowe's and Home Depot both promise to beat each other's prices by 10 percent."

Leamy also recommends stockpiling by catching "seasonal" specialties. Did you know there are spaghetti sauce wars in September between Ragu and Prego? And Quaker has sales in January, she says.

In her estimation, Leamy says, price matching can save as much as $10,000 a year in grocery costs.

"I thought people would really like to hear this," Leamy said of the book. "You want to have some pleasures in life," rather than avoiding a latte, always packing a lunch and constantly checking the tires.

So here's the Edge:

• Think about big ways to save. Leamy emphasizes a strong credit score can save you $2,916 a year on your mortgage. Raising your health insurance deductible can save $2,700.

• Price match when grocery shopping. Leamy says the Web site CouponMom.com can help you with price matching and other savings.

• Negotiate with retailers for products, banks for interest rates and car dealers for deals.

![]()

Big ideas on how to save a little money

MIKE THOMAS Staff Reporter

Elisabeth Leamy, widely known as the consumer correspondent on ABC's Good Morning America, wasn't always adept at managing her money.

While in grad school at Northwestern University's Medill School of Journalism several years ago, she sank deep into credit card debt -- partly the result, she says, of too many shopping sprees at Water Tower Place.

Now, though, her saving savvy is at an all-time high, and she shares a number of effective techniques in her new book, Save Big. Inspired by a scrappy and smart Chicago area woman Leamy had interviewed for a GMA story about America's most frugal moms, it's chock-full of insider tips on everything from mortgage shopping and car buying to healthcare and credit cards.

Why sweat the small stuff, Leamy says, when there are so many other ways to more dramatically improve your bottom line?

Q. What's been your journey from financial layperson to where you are now?

A. I have smart parents who were very much up on this stuff. And they tried to teach me, but I frankly wasn't interested. I was math-phobic. And I also, as a young woman, loved to shop.

So in college and post-college I got myself a nice credit card habit and some credit card debt. And my parents bailed me out the first time, which was mortifying. And then, you know what? I dug myself into credit card debt again. And then I dug myself out, dollar by dollar, on my own. Very proud of that accomplishment.

Right around that same time I had a secret weapon. Namely, I started dating a guy who's now my husband, and he is a certified financial planner. So I have to admit, I've had a personal tutor on some of this stuff.

Q. There are a lot of great tips in your book, but some of them will take people quite a bit more time than they're used to spending.

A. Only [on] the grocery stuff. I have a love-hate relationship with the grocery section for that very reason. It takes more regular maintenance than all my other sections. Most of the other ways to save big are things you can focus on just once every few years or few months and then you'll get a big payoff. With groceries, you do have to do more frequent work. And I don't like that about it. But on the other hand, not everybody owns a home, not everybody even owns a car.

Everybody needs groceries. And so it's kind of the baseline way to save. You can then accumulate a little bit of savings, which you can then put toward some of the other savings techniques that are even bigger.

Q. Is a smart spender the same as a good saver, or are there differences?

A. I think they're cousins. I know plenty of people who have given up their daily latte and tried to do all these other little things, but they leased a car -- which is a terrible financial mistake.

They don't carefully guard their credit to maintain the highest possible score. I say credit is a cost -- the cost of interest. I raised my score and I calculated that I've saved $116,000 in mortgage interest over the past 10 years. So people are focused on the wrong things, I believe.

Q. Why don't people make more efforts to save? Is it just not knowing how to do it?

A. Again and again, what you hear is, "Brown bag your lunch, cut out your daily latte, go to your own bank's ATM," which I agree with, but it's not always convenient. The thing is, those are all little savings.

My shtick is that I say every tip in this book has the potential to save you at least $1,000. To me, that's money to get excited about. I'm not that excited about saving $4.

Q. It's more inspirational to focus on the big stuff. There's more of a payoff. But brown-bagging it everyday, saving four bucks, adds up.

A. Brown-bagging it does add up. But I say at the end of the book that some of those little pleasures in life are what keep the big responsibilities from bumping into each other.

So I hope people won't feel stressed out on the day that they don't have time to brown bag it. And I hope people will take 15 minutes to have a coffee with a friend, which is a nice little interlude in life. I think we should enjoy some of those little pleasures.

The Consummate Consumer

By Don Oldenburg

Washington Post Staff Writer

Tuesday, May 4, 2004; Page C09

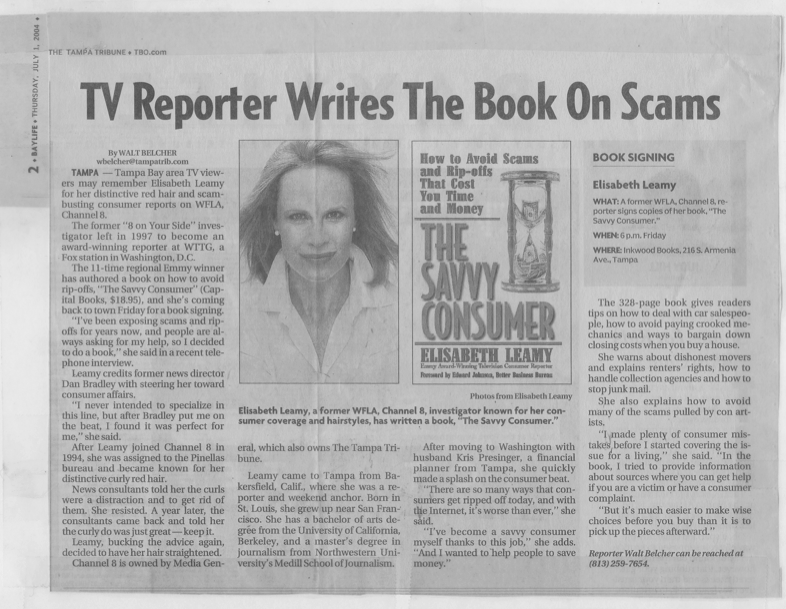

Elisabeth Leamy decided to write a how-to manual after people kept recognizing her on the street or at stores and approaching her for consumer advice.

"I realized they're hungry for this information," says Leamy, the consumer and senior investigative reporter at WTTG Fox 5 News, where she has worked for seven years.

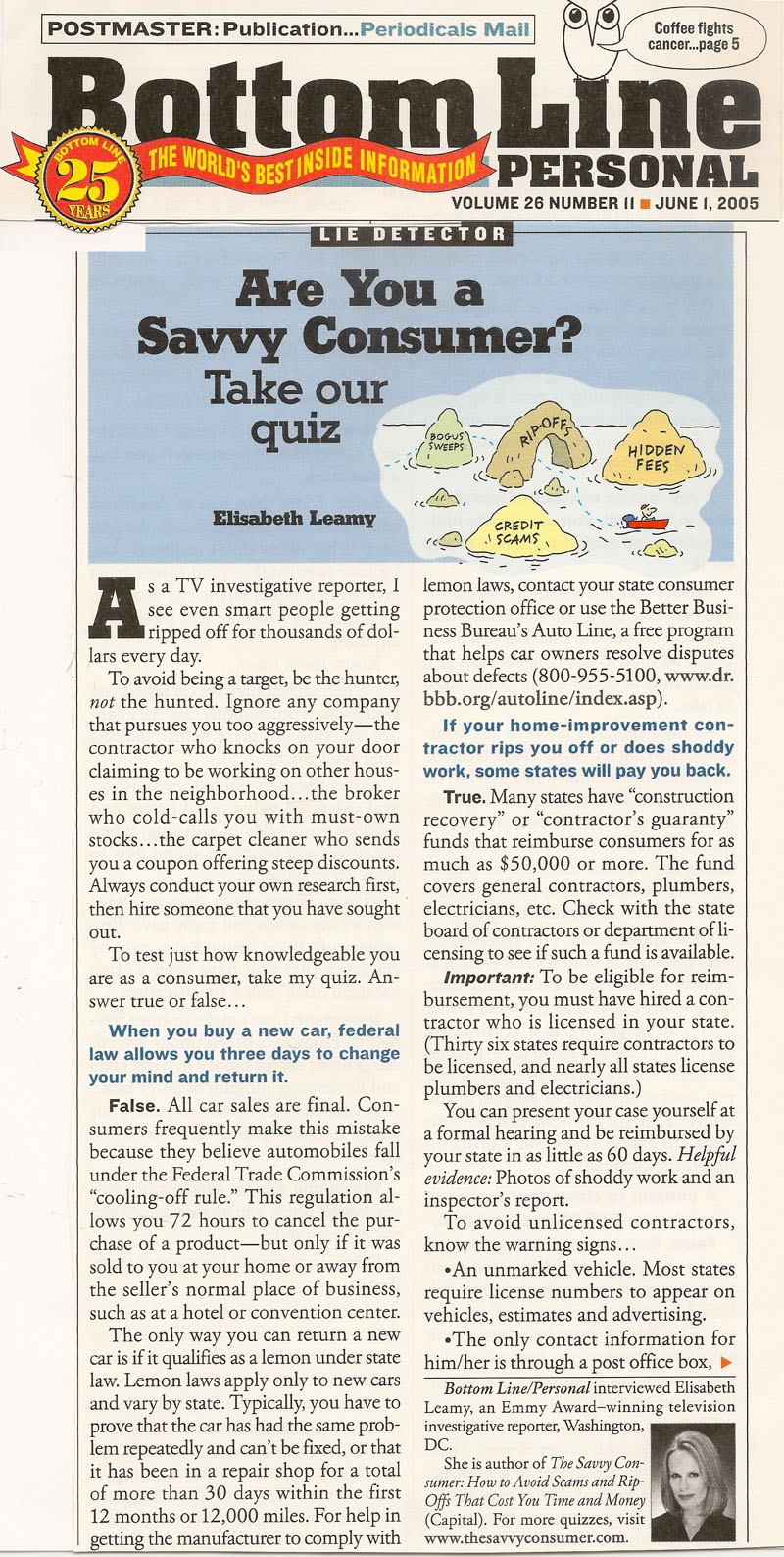

In "The Savvy Consumer: How to Avoid Scams and Rip-offs That Cost You Time and Money" (Capital Books; $18.95), she tried to answer the questions consumers asked her most. She ended up writing 340 pages on 128 topics, ranging from alarm-system and carpet-cleaning rip-offs to mortgages and pyramid schemes.

Divided into category chapters such as "Cars, "Credit" and "Telephone," the book is structured in a page-to-topic ratio that enables readers to bone up pronto on a particular issue. Most topics include tips on recognizing the telltale signs, avoiding the problem and fighting back if you didn't.

Appraisal: This book arms people with solid advice from a consumer advocate who has grappled with unreliable products, unrepentant CEOs and unlawful scammers. Why should you never buy an automobile marked "For Sale" by the side of the road? (Unlicensed dealers buy used cars by volume or at auctions, then, to jack up profits, pose as a consumer selling his personal car. It's called "curbstoning.") Want to know the average lifespan of household appliances? (Freezers, 15 to 20 years; washers, 8 to 12 years; dishwashers, 5 to 12 years.) It's here. How to tell if a prepaid calling card is a deal or a dupe? That's in it, too.

"There's always another scam or scheme, and it's exhausting to keep up with these wickedly clever con artists," says Leamy, recalling one heartbreaking case several years ago in which a grandmotherly woman was victimized by a "reloading" scheme. First, "she was scammed by a telemarketer," Leamy says, "then another con artist posed as a lawyer and pretended he would help get her money back. Of course, he stole even more of her money. She lost her life savings.

"Like bank-examiner stings and Nigerian letter scams, the reloading rip-telemarketer," Leamy says, "then another con artist posed as a lawyer and pretended he would help get her money back. Of course, he stole even more of her money. She lost her life savings."Like bank-examiner stings and Nigerian letter scams, the reloading rip-off has been around a long time. "It kills me that I hear the same tales of woe over and over again," says Leamy. "It's so easy to avoid consumer problems by doing your homework upfront. But it's excruciatingly difficult to get your money back after the fact.

"The book also tackles some widely accepted beliefs that are plain wrong. "Consumer myths continue to floor me," says Leamy. "So many people still believe they have three days to return a car once they buy it. Wrong! So many people believe the Better Business Bureau is the government agency that helps consumers. Wrong!

"Leamy's general message to consumers, reflected in almost every page: "Be the hunter, not the hunted!"

"In other words, don't do business with companies that come looking for you -- the carpet cleaner that slips a coupon under your door, the stockbroker who cold-calls you. Instead, get referrals, do a background check and do business with companies that you seek out."

The Color of Money: Michelle Singletary on women with a wealthy attitude

Michelle Singletary

February 28, 2010

Except for the occasional special coin or the Martha Washington $1 silver certificate, I always wondered why the face of a woman isn't part of U.S. currency.

Then I saw this quote from Ivy Baker Priest, a former U.S. treasurer: "Why should we mind if men have their faces on the money, as long as we get our hands on it?"

How true.

So for March, in honor of Women's History Month, I've selected four financial books written by four dynamic women for the Color of Money Book Club.

Here are the books and why I've selected them.

'A Purse of Your Own'

I simply love using a purse as a metaphor for wealth. "More than anything, the purse represents our private financial identity," Deborah Owens writes in "A Purse of Your Own." "At the end of the day, creating wealth is about adding to the purse."

Owens covers much of what you should find in this type of book. She talks about investing, saving and spending less. But she does it with a conversational tone. She's the smart sister you might wish you had and could go to for financial advice. Owens is a 20-year veteran of the financial services industry, the chief executive of Owens Media Group and the host of "Wealthy Lifestyle Radio," a personal finance talk show that airs on National Public Radio's affiliate WEAA 88.9 FM in Baltimore.

'Live It, Love It, Earn It'

Marianna Olszewski is the founder and chief executive of Madison Financial Management, a broker-dealer and hedge fund marketing company.

Her book, "Live It, Love It, Earn It: A Woman's Guide to Financial Freedom," is part motivational, part personal finance, and Olszewski seeks to first inspire before she walks you down the path to prosperity.

"A healthy mind, body and bank account are all connected," she writes.

This isn't psychobabble. Often those who are poor money managers are unhappy and unhealthy people.

Olszewski suggests you get a few of your girlfriends together and read the book as a group to follow her exercises. "The power of the tools is enhanced, and abundance comes to all of us much more quickly than if we are working on them by ourselves."

'Save Big'

I'm a lifelong penny-pincher who follows the cautionary advice from Benjamin Franklin that "a small leak will sink a great ship." I use this quote to drive home to people that it's the small expenditures in life that can add up to big losses.

But in "Save Big," Elisabeth Leamy, who is a consumer correspondent for ABC's "Good Morning America," says to buy your latte in the morning and work on spending less on the big stuff.

Her personal finance philosophy: "I've always preferred to save a lot of money on a few things rather than a little bit of money on a bunch of things. I like to save big. Not small."

Every tip in her book has the potential to save you at least $1,000, she says. She shows you how to save on the five things we spend the most on -- a home, car, credit card, groceries and health care.

'Expect to Win'

Wall Street veteran Carla A. Harris is a managing director at Morgan Stanley Investment Management, and her book "Expect to Win" has a lot of sage and specific advice if you need a push to the top of the career ladder.

I know we're in a recession, so I'm not suggesting you buy all four books -- unless you can truly afford to. But at least put them all on your list to read eventually because each has something to offer and will help you, as Priest, the former treasurer, says, get your hands on some money.

It's easy to be a member of the Color of Money Book Club. We don't meet, at least not in person. We come together for a live online discussion. Join me at noon March 25 at http://washingtonpost.com/discussions. All four authors of this month's selected books will be available to take your questions. And, yes, gentlemen are welcome.

Every month, I randomly select readers to receive a copy of the featured book, donated by the publisher. This month, I'll be giving away copies of all four books.

For a chance to win one of them, e-mail colorofmoney@washpost.comwith your name and address. Please identify which book you would like in the subject line of your e-mail.

Readers can write to Michelle Singletary at The Washington Post, 1150 15th St. NW, Washington, D.C. 20071.

Comments and questions are welcome, but because of the volume of mail, personal responses are not always possible. Please note that comments or questions may be used in a future column, with the writer's name, unless a specific request to do otherwise is indicated.

![]()

“Woman's World!”

Kristina Mastrocola

From zeroing in on lost treasure to making a few extra dollars on the side, our savvy panel of financial pros share painless ways to put more cash in your pocket!

Read the whole article here

![]()

These books bring financial matters into better focus

Gail MarksJarvis

How about buying a book for a holiday gift?

It's easy and affordable. You can shop from home, and the person who receives the book can fulfill the new pastime of entertaining themselves frugally at home.

Here are some suggestions to educate people about the harrowing financial crisis or enable them to make the most out of their money in a tough economy. Some of my favorite personal finance books were released prior to this year, so before heading to the bookstore, make a phone call or search online.

Disaster insight. Among the many books just released, two good reads are Gillian Tett's "Fool's Gold" and Andrew Ross Sorkin's "Too Big to Fail." Tett, an anthropologist turned financial journalist for the Financial Times, focuses on a Wall Street culture that resulted in disaster. Sorkin, a New York Times reporter, looks inside the private meetings in which Wall Street and the government's elite determined our financial fate during the crisis.

Two professors who have spent years studying the world's various financial crises put the recent blunders and challenges into historical perspective. Check out "This Time is Different: Eight Centuries of Financial Folly," by Carmen Reinhart and Kenneth Rogoff.

What makes us tick? Although some predict that "shop till you drop" is dead, Lee Eisenberg's "Shoptimism: Why the American Consumer Will Keep on Buying No Matter What" is an enjoyable look into what drives people to buy. Jason Zweig, in "Your Money & Your Brain: How the New Science of Neuroeconomics Can Help Make You Rich," will make you aware of how your brain can cause you to invest poorly and how to fix it.

Starting out right. Help friends and family handle their financial lives effectively so they can make the most of their money. Beth Kobliner's "Get a Financial Life: Personal Finance in Your Twenties and Thirties" is one of my favorite wedding or graduation gifts because it walks young adults through every financial decision, from mortgages to credit cards, bank fees, insurance and investing. For people of all ages, Liz Pulliam Weston's "Deal with Your Debt" illustrates how to escape debt, and her "Easy Money" shows how to handle money simply and effectively.

Save on everything. With frugality so popular, many books provide tips on cutting costs on everything from utilities to groceries. Elisabeth Leamy's "Save Big: Cut Your Top 5 Costs and Save Thousands" is invaluable because it focuses on big expenses, including mortgages, cars and insurance, and makes each step understandable.

Need a job? If you know someone who's having trouble landing an interview, Jeffrey Allen's "Instant Interviews: 101 Ways to Get the Best Job of Your Life" introduces a gutsy, creative approach.

Ready to retire? Many books are too generic or don't walk you through details needed to figure out if you have enough money to retire and how to not run out. "Spend 'til The End," by Laurence Kotlikoff and Scott Burns, is essential for anyone who wants to stretch retirement savings. Also helpful: Julie Jason's "The AARP Retirement Survival Guide."

Paying for college. An essential book for anyone who cannot afford the full cost of sending children to college is Kalman Chany's "Paying for College Without Going Broke." It provides financial aid strategies that can provide thousands of dollars in free assistance. It's essential reading for parents with sophomores and juniors in high school.

For Jim Cramer fans. If you know a fan of Jim Cramer's "Mad Money" TV show who buys stocks solely on his tips, they are taking risks that Cramer himself wouldn't endorse. He suggests putting at least an hour of work a week into researching stocks. His books tell people how. His latest is "Jim Cramer's Getting Back to Even."

If you know someone willing to read an investing classic, try Benjamin Graham's "The Intelligent Investor."

How to Save on Big-Ticket Items

Kimberly Palmer

March 31, 2010

To Elisabeth Leamy, Good Morning America's consumer correspondent, pinching pennies by skipping coffee or bringing lunch to work is barely worth the trouble. (She says she ends up eating her bagged meal by 11 a.m. and buying a second one in the midafternoon, anyway.) Plus, she likes supporting the local coffeehouse with her green tea habit. She also likes saving money—but only when she can save a lot of it.

That's why she tells people how to save thousands of dollars at once, instead of a few bucks here and there, in her new book, Save Big: Cut Your Top 5 Costs and Save Thousands! By negotiating with everyone from real estate agents to doctors to grocery stores, Leamy estimates that she shows readers how to save close to $2 million—more than the cost of all of the lattes anyone could safely drink.

[Slide Show: How to Save on Big-Ticket Items.]

Plus, she notes, many people are already pinching pennies but are still struggling to spend less than they bring in. "Little things aren't enough right now," she says. "People tell me that they're skipping lattes but are paying bills late, and that slams your credit score, and then you pay much more than you would otherwise," she says.

Leamy focuses on five big-ticket areas: homes, cars, credit, groceries, and healthcare.

Buy a house, but pay fewer fees. Leamy points out that generally speaking, buying a home allows people to save a lot of money, because it forces them to save by investing in their home each time they write a mortgage check. Plus, homeowners receive tax benefits unavailable to renters. To keep as much money as possible in your bank account, she recommends negotiating discounts with your Realtor, lender, and settlement company.

Real estate agents, for example, are often willing to accept a 2 percent fee instead of the traditional 3 percent, especially if house hunters do much of the work themselves. As for lenders and settlement companies, they will often cut buyers a break on various fees, such as application fees or document preparation fees, if asked.

"Negotiating in our culture is always a little awkward, but some of these dollar amounts are too big to let embarrassment get in the way," says Leamy. Plus, she says, mortgage professionals are increasingly getting used to it these days.

Stick to used cars. New cars lose so much of their value in the first few years of ownership that they're not worth purchasing, Leamy says, especially when you can buy a certified used car that will last. "Cars these days are really well built, so the risk is lower than it used to be," she says. Leamy suggests investing time in the research phase of your purchasing process so you're sure to buy a reliable vehicle. In fact, she even says it's worth paying extra on the car to increase the chances you're getting a good one.

Leamy also recommends bringing cash to the dealership to avoid paying interest on a car loan. "Paying interest on something that is definitely going down in value is a horrendous waste of money," she says.

Defend your credit. Keeping a clean credit report—and high credit score—means you'll pay less for any type of loan you take out, including massive mortgages. That's why Leamy suggests ordering your free credit report once a year through annualcreditreport.com to make sure it is correct. If you're taking out a $250,000 mortgage, for example, a credit score of 785 instead of 635 could potentially save you $87,480 over 30 years, depending on prevailing interest rates.

[See Credit Card Fees: 5 Things You Should Know.]

Keep a grocery stash. By stockpiling groceries, you'll not only be able to purchase more items when they're on sale and save them for later (just stick meat and bread in the freezer), but you'll also be able to make use of Leamy's other big idea: Skip shopping trips. She says that many people can get by on the food they already have for a week, so why not skip shopping once a month or once a quarter? If you're used to shopping very week and spending $7,500 a year, then skipping the trip once a month could save you $1,800, or 24 percent of your annual grocery bill.

Cut deals with doctors. Just like real estate agents, doctors are getting increasingly used to patients who want to bargain with them—and making the effort is worth it, says Leamy. By asking doctors for discounts upfront, especially if you're willing to pay for their services with cash, you might be able to get as much as 50 percent off your medical bills.

Then you'll be able to afford a latte after your visit.

http://www.parents.com/parenting/money/taxes/tax-deductions-parents-should-know/

Everyone wants to save money, and parents are no exception. But when it comes to filing taxes, did you know there are certain tax breaks that apply just for parents? Even if you feel like you're spending more than saving, having a child can actually help you save some cash during this tax season.

As much as we love our children, having kids often feels like a bottomless money pit. But there is some relief for overburdened parents.Uncle Sam knows just how costly it is to have a baby, so there are a number of tax breaks and deductions parents can claim on their returns. Here are the ones to make sure you're covered in your taxes this year.

1. Child tax credit. Moms and dads can claim $1,000 per household child up to age 17, according to Ellie Kay, a Parentsadvisor for the Mom Money Clinic and a family financial expert. But once a couple's adjusted gross income is $110,000 or more (or $75,000 for single parents), that perk is no longer an option.

2. Earned income tax credit (EIC). Parents of three or more children who have earned less than $46,997 for the year if they're single or less than $52,427 if they're married can take this credit, Kay says. Very low-income parents of one or two kids can also qualify. The maximum EIC allowed is $6,143.

3. Child-care deductions and pretax accounts. Working parents who pay for child care might be able to deduct some of those costs from their taxes, according to Elisabeth Leamy, a money expert and consumer correspondent for The Dr. Oz Show. The amount is based on income and is between $600 and $1,050 in savings a year per child. For licensed day-care centers and after-school programs or qualified babysitters with social security numbers, parents can get a dependent care tax credit of up to 35 percent of the cost of that care. Keep in mind that there's a $6,000 maximum for two or more family members and a $3,000 cap per child. Another way to go, if your employer offers it as a benefit, is to put money into a flexible spending account, or FSA, for child-care costs, which allows up to $5,000 in contributions that aren't taxed. But, Leamy notes, parents can't take advantage of both an FSA and the child care credit; they have to choose one or the other.4. Medical expenses deductions and pretax accounts. Total family health care expenses that exceed 7.5 percent of the household's adjusted gross income can be deducted from your taxes, according to Kay, including things like physical therapy and dental care but excluding insurance premiums. Or parents can invest in their employers' Health Spending Accounts (HSAs), which, like FSAs, allow pretax contributions of up to $5,000 a year.

5. College savings plan deductions. If you've opened a 529 plan account or started another state-sponsored college fund for your child, any contributions made in 2014 can be claimed as deductions on your state taxes.

6. Adoption tax credit. Parents who finalized adoptions in 2014 are eligible for up to $13,190 per child in federal tax credits. "A little caution, though: Make sure you have all the paperwork," Kay advises. "Adoptions can be drawn out, so if [the adoption] was not finalized in 2014, that could be a problem." At the very least, though, the credit would be postponed by a year.

7. Dependent tax exemption. When you're single, you can claim one exemption; when you're married, you get two; and when you have kids, you get one for each child, Leamy says. That amounts to $3,950 per person for 2014. Since this is a deduction rather than a credit, the savings is based on your tax bracket. For example, those in the 25 percent bracket will save $975 with the exemption.

http://www.parents.com/parenting/money/taxes/tax-tips-for-new-parents/

When you're a new parent, everything is overwhelming -- from figuring out how take care of your new baby to figuring out how to file your taxes with the new household addition. Luckily, here's a cheat sheet on what you should know when getting your paperwork together for tax season.

By Catherine Donaldson-Evans

It goes without saying, but having a baby isn't cheap -- a fact that often blindsides new parents."New parents don't have a lot of extra money, and having a baby is a lot more expensive than they think it would be," says Ellie Kay, a Parents advisor for the Mom Money Clinic and a family financial expert. "I say that as the mother of seven."With all the extra items to check off the to-do list once an infant joins the family, doing taxes is probably the last thing on a sleep-deprived mom or dad's mind. But by following these basic tax tips, couples who had a child in 2014 can save themselves quite a bit of money, which could be a lifesaver in these strapped-for-cash times.

1. Make sure your child has a social security number. Applying for one usually happens at the hospital right after the baby is born, but in some extenuating circumstances, filing the paperwork gets put off, Kay says. The only way for the government to honor all the deductions and credits new parents can claim is to confirm the child's birth, which is why the baby's social security number is so crucial.

2. File taxes early rather than wait until the last minute. This is no easy feat for busy new parents, but it's important. "Even though you might use a tax software or an accountant, human errors can still happen," Kay says. "When you're in a rush, you tend to make errors. That can add up to between several hundred and several thousand dollars on your tax return."

3. Have all your receipts in order. Collecting receipts might seem daunting with all the chaos that comes with having a baby, but if you've been filing them all year long, it should be doable to round them up at tax time. And you'll need them for any deductions you're claiming. "Have a good paper trail," Kay advises. "And if you've kept a digital paper trail, make sure you have it backed up."

4. Change your W-4. Consider filling a new W-4 that reduces how much is being withheld from your paycheck in taxes, suggests Elisabeth Leamy, a money expert and consumer correspondent for The Dr. Oz Show. "Now that you've got a dependent, child credits and deductions mean you're not going to owe as much at tax time, so you don't have to prepay as much tax throughout the year," she says.

5. Use a cash-back credit card to save a little extra money. "Money saved is tax-free," Leamy says. "Make saving money a goal. For exhausted new parents, a simple way to save is by using a cash-back credit card." She recommends the Citi Double Cash card, which gives 1 percent cash back when cardholders make a purchase and another 1 percent when they pay for it.

6. Start saving for your child's college now. It's never too early to put money aside for your child's college fund, according to both Leamy and Kay. Open a 529 plan account, which accumulates money for college tax-free and can be claimed as a deduction on your taxes. Or try investing in a Coverdell Education Savings Account (ESA), Leamy advises. The money is also not taxed, and parents can contribute up to $2,000 a year.